7 Phrases That Quietly Kill Your Investor Pitch

![7. "This is a no-brainer for [customer type]"](https://assets.supramono.com/products/infrairis/explainer/explainer-268-slide-7-adjust-b932aee2.png)

You've rehearsed the deck. You know your numbers. You genuinely believe the product is fundable. Then the room goes quiet in a way that isn't good, and you spend the drive home trying to work out what happened.

Most of the time, it wasn't your product. It was your language.

Investors make pattern-recognition decisions faster than most founders realise. DocSend's deck analytics have consistently shown that first-pass deck review times are measured in minutes, not hours — and that decks which don't secure funding are often closed faster than those that do. In a live pitch, the spoken opening has similarly limited runway. The harsh reality of modern fundraising is that founders have less time than ever to make an impression, and investors will decide within roughly two minutes whether your pitch deserves deeper consideration.

That means the first few sentences you say — before a single financial model is examined — are doing more work than founders typically give them credit for. Early information shapes overall perception: investors often rely on the early parts of what they hear to interpret everything that follows, which is why starting strong is crucial to ensuring they view the rest through a positive lens.

Ambiguous, inflated, or hedged language doesn't just fail to impress. It actively triggers scepticism. Experienced investors have heard thousands of pitches, and they've developed sharp instincts for the phrases that signal an underdeveloped business case. Investors are constantly looking for shortcuts to assess credibility, and signals help them form judgments quickly in an environment where they must evaluate hundreds of pitches a year.

Here are seven phrases that quietly kill pitches — and what to say instead.

1. "We're disrupting the [industry] space"

The word "disruptive" has been stripped of all meaning. In the experience of most pitch coaches and investors, terms like "paradigm shift" or "disruptive technology" are so overused that any signal value has been lost. Investors stopped reacting to it years ago. What they hear now is: this founder hasn't found a precise way to describe what they actually do.

The problem isn't ambition. It's the abstraction. "Disruption" tells an investor nothing about your mechanism of action, your beachhead customer, or why you win. It's a conclusion without a case.

Replace it with the specific dynamic you're changing. If your B2B SaaS product cuts compliance audit prep time from six weeks to three days for financial services firms, say exactly that. The number does the disruption claim's job, without the eye-roll.

2. "AI-powered" (as the headline claim)

Founders in non-AI sectors often feel invisible, so they start adding AI language to their pitch even when the feature is minor. This is a mistake. Investors can smell label engineering. And in 2026, with AI-related deals accounting for a growing and disproportionate share of global venture activity — some trackers have placed the figure above 40% of deal value in recent quarters, though estimates vary by geography and methodology — the term has become difficult to use as a differentiator without more specificity.

Saying your product is "AI-powered" without specifying the mechanism tells an investor nothing about your moat. Are you fine-tuning a foundation model? Running proprietary inference pipelines? Using off-the-shelf APIs with a thin wrapper? Sophisticated investors are wary of AI's speed-to-commoditisation, and the pitches that get follow-up meetings explain, concretely, why their solution will maintain an edge.

If AI is genuinely core to your product, describe the specific capability it enables that wasn't possible before. "Our model processes histopathology slides in 40 seconds with 94% diagnostic concordance" is fundable. "AI-powered diagnostics" is wallpaper.

3. "There's no real competition"

This one doesn't just trigger scepticism. It ends the pitch quietly in the investor's head while they're still smiling politely at you.

Don't claim no competition anywhere in your deck. At best, it will be seen as an exaggeration — if there isn't direct competition, there may be indirect competition to consider. At worst, it could make investors think you haven't fully explored the market, meaning your entire premise could be flawed.

Every product competes with something, including the status quo. The spreadsheet. The manual process. The incumbent vendor whose product is terrible but embedded. Even if you're first to market in a new space, identify the status quo alternative — that's the real opportunity statement.

Saying "we have no competition" doesn't signal confidence. It signals that you haven't done the market analysis an investor will run in their first due diligence call. Get ahead of it. Name your alternatives, explain the specific dimension on which you win, and move on.

4. "We think this could be big" (and other hedging phrases)

"We think," "hopefully," "we believe this might," "sort of" — hedging language is disproportionately penalised in high-stakes conversations. Not because investors expect founders to be certain about everything. They don't. They're backing founders to navigate uncertainty.

What hedging communicates is something different: that the founder isn't yet committed to the claim they're making. Investors want to feel that the founder is not only smart but hungry, driven, and deeply connected to their mission. A founder who conveys indifference about outcomes rarely inspires commitment.

The fix isn't false certainty. It's specificity. "We think the market could be large" is weak because it's vague. "Our initial target is the 4,200 mid-market financial services firms in ANZ that still run compliance audits manually — we've closed 11 of them in six months" is confident because it's grounded. You're not claiming the whole ocean. You're showing exactly which part of the ocean you're already fishing in.

Research in organisational behaviour and linguistics has explored how jargon functions as a status signal — and how, in certain contexts, it can backfire. In a pitch setting, leaning heavily on terms like "leverage" or "disrupt" can read as a substitute for substance rather than evidence of expertise. This observation, shared by many pitch coaches, is that founders who reach for jargon in investor conversations often do so when they're least confident in the underlying claim.

5. "We're targeting a $50 billion market"

Large TAM numbers aren't inherently a problem. Investors do want to back companies with meaningful upside. But inflated market sizing — especially when it arrives unsupported and enormous — functions as a credibility leak.

Founders often quote a massive TAM number from a Google search and assume investors will be impressed. They won't. Investors have seen the "$500 billion market opportunity" slide a thousand times. What impresses them is a realistic SOM backed by logic.

The issue is that a huge TAM without a credible path through SAM and SOM tells an investor that you don't yet understand your actual go-to-market. It signals top-down thinking rather than bottom-up validation. And once an investor starts doubting one piece of your analysis, they fill the gaps in the story with their own, usually sceptical, assumptions.

Work from the bottom up. Identify the specific customer segment you're going after first, the number of qualifying buyers, and what you can realistically close in the next 12 months. The math will still produce a compelling number, and it will actually be believed.

6. "We have first-mover advantage"

This phrase has a specific failure mode. It sounds like a moat. Investors hear it as an absence of one.

In most cases, citing first-mover advantage without explaining the mechanism that makes it durable will be dismissed by sophisticated investors. Research by Lieberman, Montgomery, and others in the strategy literature shows that first-mover advantage is highly context-dependent: it tends to hold where being first directly enables defensible asset accumulation — proprietary data, high switching costs, network effects, or exclusive contracts. Where those mechanisms are absent, a better-funded competitor can often close the gap quickly. The exception is when first-mover timing is inseparable from a specific moat — in which case the mechanism, not the timing, is the argument to make.

Being first is a timing observation, not a defensibility argument. What matters is why being first translates into a durable advantage: proprietary data you're accumulating, switching costs you're building, network effects that compound, contracts that create exclusivity. Those are moats. "We were first" is just a historical fact that a better-funded competitor can potentially negate quickly.

If you have genuine defensibility, describe the mechanism, not the timing. "Our platform has ingested 47 million de-identified patient records under exclusive data agreements with three hospital networks" is a moat. "We're the first to market" is a starting gun.

7. "This is a no-brainer for [customer type]"

This phrase fails on two levels. First, it's an assertion that substitutes for evidence. Second, in the experience of many pitch coaches, calling something a "no-brainer" can come across as dismissive of the real friction customers face in making a purchasing decision.

More importantly: if it were genuinely a no-brainer, the customer would already have bought it. The fact that you're in a funding pitch means you need capital to acquire customers, which means acquisition isn't as effortless as the phrase implies. A smart investor will notice that contradiction immediately.

The substitute is evidence of buying behaviour. How many customers have already bought? How long did their sales cycle take? What was the primary objection and how did you overcome it? What's your current NRR? Retention metrics and net dollar retention trends show not just initial interest but ongoing customer engagement and revenue stability, and investors increasingly view retention as a stronger indicator of product-market fit than short-term growth.

How one bad phrase derails the whole room

Here's the thing about investor conversations that makes language so high-stakes: confusion compounds.

When an investor hears a phrase they can't attach to a concrete mechanism — "disruptive AI-powered solution" is the canonical example — they don't silently file a note and move on. They ask a clarifying question. That question pulls you off your narrative arc. Your answer, if it's improvised, may introduce a new ambiguity. Now there's a second question. By the fourth slide, you're no longer pitching. You're defending.

The human brain remembers stories better than data points. While facts and figures are essential, you can enhance their impact with a compelling narrative — a pitch that tells a clear, engaging story is much more likely to resonate with investors. When unclear language triggers a question that interrupts the arc, the story never gets finished. What the investor remembers is confusion, not the product.

This is why the highest-performing pitches aren't the simplest ones. They're the most precise ones.

The antidote isn't simplification. It's precision.

There's a common piece of advice given to deep tech founders: "simplify your pitch." It's not wrong, but it's incomplete. The founders who consistently close rooms don't strip out the complexity — they replace fuzzy language with specific mechanisms.

Among the most effective pitch hooks are those that compress the whole thesis into a single short phrase — the kind an investor can repeat to a colleague. But that phrase has to be earned through precision, not achieved through vagueness.

For every phrase you're currently using in your pitch, ask one question: what is the specific, verifiable thing this phrase is trying to communicate? If you can answer that question, say the answer instead of the phrase. "AI-powered" becomes "our model reduces false positive rates by 73% versus the clinical standard." "Disruptive" becomes "we deliver in three weeks what traditional agencies take three months to produce." "No-brainer" becomes "eleven customers have renewed at 140% NRR after six months" — these are illustrative examples of the kind of specificity that replaces vague claims, not references to a real company.

Investors are asking harder questions about margins, distribution, defensibility, and time to revenue. The founders who answer those questions before they're asked, in the language of mechanisms and outcomes rather than superlatives and adjectives, are the ones who walk out with term sheets.

Make every slide count by including specific data points, exact dates, quantified metrics, and clear attribution to credible sources that stand up to scrutiny during the investment evaluation process.

That standard applies to every word too, not just every slide.

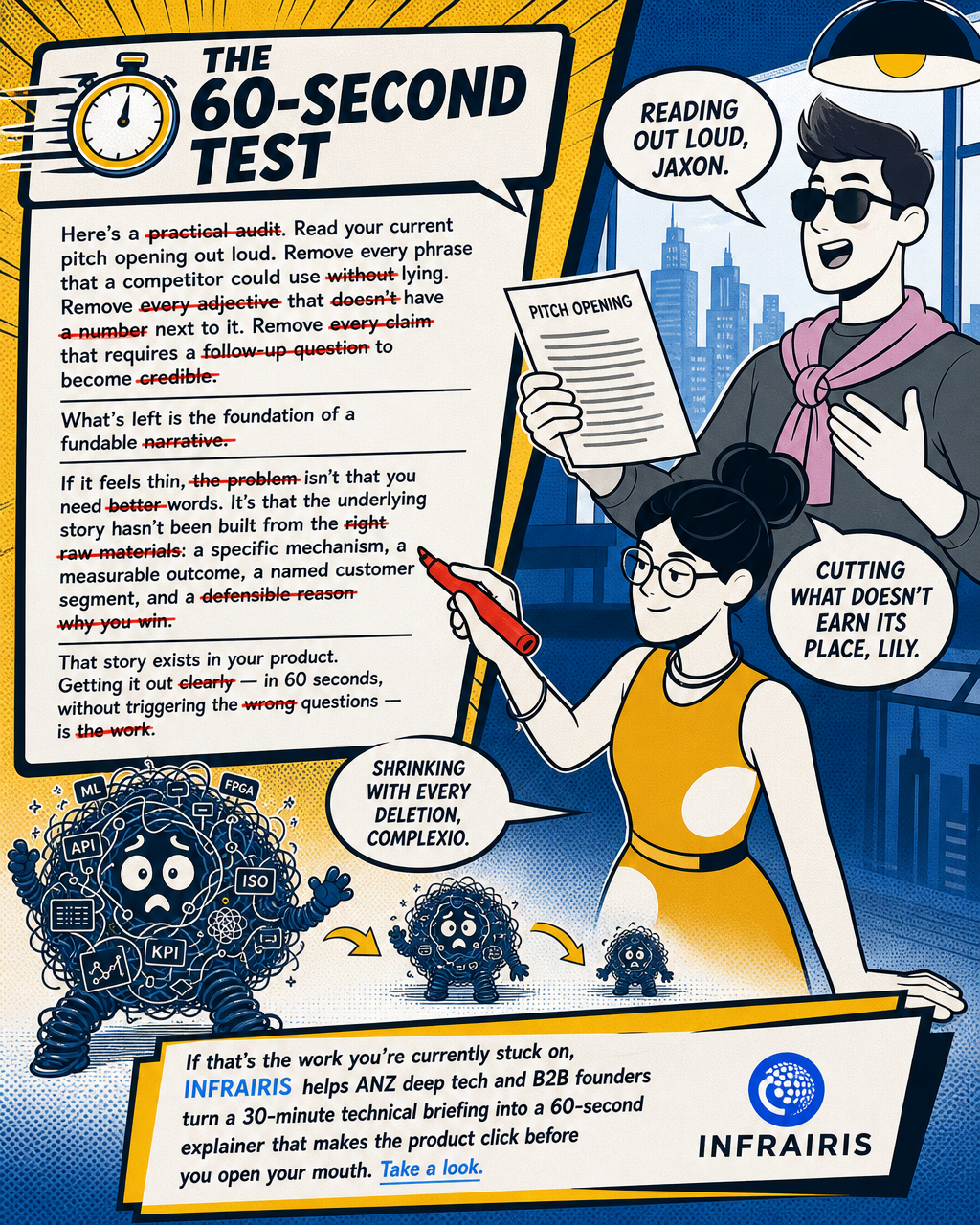

The 60-second test

Here's a practical audit. Read your current pitch opening out loud. Remove every phrase that a competitor could use without lying. Remove every adjective that doesn't have a number next to it. Remove every claim that requires a follow-up question to become credible.

What's left is the foundation of a fundable narrative.

If it feels thin, the problem isn't that you need better words. It's that the underlying story hasn't been built from the right raw materials: a specific mechanism, a measurable outcome, a named customer segment, and a defensible reason why you win.

That story exists in your product. Getting it out clearly — in 60 seconds, without triggering the wrong questions — is the work.

If that's the work you're currently stuck on, Infrairis helps ANZ deep tech and B2B founders turn a 30-minute technical briefing into a 60-second explainer that makes the product click before you open your mouth. Take a look.

Related reading

Infrairis

Your complex product. In 60 seconds. Clearly.

Your complex product. In 60 seconds. Clearly.

Learn more about Infrairis and get started today.

Visit Infrairis